Yves here. This is an interesting theory, but I’m not sure I buy it. McEndree’s argument is basically that US shale players weren’t the main target of the Saudis because they haven’t succeeded in lowering their production. The fact that the effort so far has not worked as perhaps planned isn’t proof that it wasn’t the Saudis’ aim, particularly since they said at the very outset that they as the low cost producer, should not be the swing producer.

Note I find the “main target” to be a bit of a straw man, since even at the time of the Saudi refusal to cut production to support prices, many observers (including yours truly) argued the Saudis were targeting not just the US but all higher cost producers, including its geopolitical enemies like Russia and Iran.

The mistake of the Saudis (and most oil analysts) was one not made by John Dizard of the Financial Times. Dizard correctly predicted that the shale players would keep pumping as long as they had access to financing. Indeed, as we’ve seen, they are continuing to pump strictly to keep servicing debt. And the need to produce revenues (which is the motivation for most major oil producing nations, since they need oil income to finance their national budgets) means all the producers are locked into a bad equilibrium: they are all going to keep producing at levels higher than the markets can absorb until either a deal or an external force makes them stop. With the frackers, it will be access to financing.

And what I believe McEndree also misses, but I welcome informed criticism if I have this wrong, is that fracking won’t be so easily resumed once fracking companies start hitting the wall and/or defaulting. Their old business model presupposed much higher prices and high leverage. I doubt we’ll see prices above $60 a barrel, nor will we see anywhere near as much gearing of shale gas plays as in the past. How many fields are economically viable if one assumes the odds don’t favor oil over $60 for at least the next few years, much higher levels of equity financing, and you also factor in your required equity return greater regulatory risk (curbs or outright ban in some areas due to earthquake risk and the impact on water supplies)?

By Dalan McEndree, whose career has focused on the Soviet Union and Russia, and has included fifteen years in Russia as a U.S. diplomat, in business, working both for international and Russian businesses, and in consulting. Originally published at OilPrice

Do the Saudis have an oil market strategy beyond pumping crude to defend their market share? Are they indifferent to which countries’ oil industries survive? Or, alternatively, are they targeting specific global competitors and specific national markets? Did they start with a particular strategy in November 2014 when Saudi Petroleum and Mineral Resources Minister Ali al-Naimi announced the new market share policy at the OPEC meeting in Vienna and are they sticking with it, or has their strategy evolved with the evolution of the global markets since?

And, of course, what does the Saudi strategy beyond pumping crude portend for the Saudi approach to some OPEC members’ calls for coordinated production cuts within OPEC and with Russia?

Conventional Wisdom

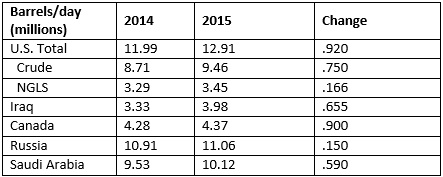

Conventional wisdom has it that the Saudis are focused primarily on crushing the U.S. shale industry. In this view, the Saudis blame the U.S. for the supply-demand imbalance that began to make itself felt in 2014. U.S. production data seems to support this. Between 2009 and 2014, U.S. crude and NGLs output increased nearly 4 million barrels per day, while Saudi Arabia’s increased only 1.64 million barrels per day, Canada’s 1.06 million, Iraq’s 0.9 million, and Russia’s 0.7 million (Saudi data doesn’t include NGLs).

In addition, the Saudis, among many others, believed that U.S. shale would be the most vulnerable to Saudi strategy, given relatively high production costs compared to Saudi production costs and shale’s rapid decline rates and the need therefore repeatedly to reinvest in new wells to maintain output.

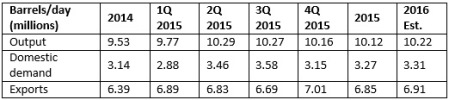

Yet, if the Saudis were focused on the U.S., their efforts have been unsuccessful, at least in 2015. As the table below shows, U.S. output growth in 2015 outstripped Saudi output growth and the growth of output from other major producers in absolute terms. In addition, many observers also came to believe that U.S. shale production will recover more quickly than production in traditional plays once markets balance due to its unique accelerated production cycle and that this quick recovery will limit price increases when markets balance.

Is the U.S. Really the Primary Target?

The above considerations imply the Saudis—if indeed they primarily were targeting U.S. shale—embarked on a self-defeating campaign in November 2014 that could at best deliver a Pyrrhic victory and permanent revenues losses in the US$ hundred billions.

Is the U.S. the primary target? U.S. import data (from the EIA) suggests the U.S. is not now the Saudis’ primary target, if it ever was. Like other producers, the Saudis operate within a set of constraints. Domestic capacity is one. In its 2015 Medium Term Market Report (Oil), the IEA put Saudi Arabia’s sustainable crude output capacityat 12.34 million barrels per day in 2015 and at 12.42 million in 2016. Export capacity—output minus domestic demand—is another.

Rather than maintaining crude output at 2014’s level in 2015, the Saudis steadily increased it after al-Naimi’s announcement in Vienna as they brought idle capacity on line (data from the IEA monthly Oil Market Report):

This allowed them to increase average daily crude exports by 460,000 barrels in 2015 over 2014 average export levels—even as Saudi domestic demand increased—and exports peaked in 4Q 2015 at 7.01 million barrels per day (assuming the Saudis keep output at average 2H 2015 levels in 2016, and domestic demand increased 400,000 barrels per day, as the IEA forecasts, the Saudis could export nearly 7 million barrels per day on average in 2016):

The Saudis did not ship any of their incremental crude exports to the U.S.—in other words, they did not increase volumes exported to the U.S., did not directly seek to constrain U.S. output, and did not seek to increase U.S. market share. Based on EIA data, Saudi imports into the U.S. declined from 1.191 million barrels per day in 2014 to 1.045 million in 2015—and have steadily declined since peaking in 2012 at 1,396 million barrels per day. (OPEC’s shipments also declined from 2014 to 2015, from 3.05 million barrels per day to 2.64 million, continuing the downward trend that started in 2010). Canada, however, which has sent increasing volumes to the U.S. since 2009, increased exports to the U.S. 306,000 barrels per day in 2015:

Also, the Saudi share of U.S. crude imports declined 1.9 percentage points in 2015 from 2014, and has declined 2.6 percentage points since peaking at 16.9 percent in 2013; during the same two periods, Canada’s share increased 4.5 and 9.9 percentage points respectively (and has more than doubled since 2009):

Other Markets

The Saudis presumably exported the incremental 606,000 barrels per day (460,000 from net increased export capacity plus 146,000 diverted from the U.S.) to their focus markets. Since other countries’ import data generally is less current, complete, and available than U.S. data, where these barrels ended up must be found indirectly, at least partially.

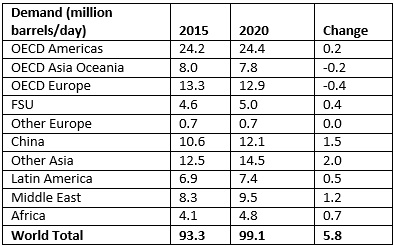

In its 2015 Medium Term Market Report (Oil), the IEA projected that the bulk of growth from 2015 to 2020 will come in China, Other Asia, the Middle East, and Africa, while demand will remain more or less stagnant in OECD U.S. and OECD Europe:

The Saudis find themselves in a difficult battle for market share in China, the world’s second largest import market and the country in which the IEA expects absolute import volume will increase the most through 2020—1.5 million barrels per day (it projects Other Asia demand to increase 2.0 million). The Saudis are China’s leading crude supplier. However, their position is under sustained attack from their major—and minor—global export competitors. For example, through the first eleven months of 2015, imports from Saudi Arabia increased only 2.1 percent to 46.08 million metric tons, while imports from Russia increased 28 percent to 37.62 million, Oman 9.1 percent to 28.94 million, Iraq 10.3 percent to 28.82 million, Venezuela 20.7 percent to 14.77 million, Kuwait 42.6 percent to 12.68 million, and Brazil 102.1 percent to 12.07 million.

As a result of the competition, the Saudi share of China’s imports has dropped from ~20 percent since 2012 to ~15 percent in 2015, even as Chinese demand increased 16.7 percent, or 1.6 million barrels per day, from 9.6 million in 2012 to 11.2 million in 2015. Moreover, the competition for Chinese market share promises to intensify with the lifting of UN sanctions on Iran, which occupied second place in Chinese imports pre-UN sanctions and has expressed determination to regain its prior position (Iran’s exports to China fell 2.1 percent to 24.36 million tons in the first eleven months of 2015).

Moreover, several Saudi competitors enjoy substantial competitive advantages. Russia has two. One is the East Siberia Pacific Ocean pipeline (ESPO) which directly connects Russia to China—important because the Chinese are said to fear the U.S. Navy’s ability to interdict ocean supplies routes. Its capacity currently is 15 million metric tons per year (~300,000 barrels per day) and capacity is expected to double by 2017, when a twin comes on stream. The second is the agreement Rosneft, Russia’s dominant producer, has with China National Petroleum Corporation to ship ~400 million metric tons of crude over twenty-five years, and for which China has already made prepayments. Russia shares a third with other suppliers. Saudis contracts contain destination restrictions and other provisions that constrain their customers’ ability to market the crude, whereas those of some other suppliers do not.

Marketing flexibility will be particularly attractive to the smaller Chinese refineries, which Chinese government has authorized to import 1 million-plus barrels per day.

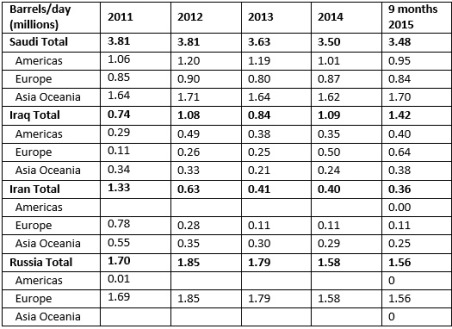

While they fight for market share in China, the Saudis also have to fight for market share in the established, slow-growing or stagnant IEA-member markets (generally OECD member countries). Saudi exports to these markets declined 310,000 barrels per day between 2012 and 2014, and 490,000 barrels per day between 2012 and 2015’s first three quarters. Only in Asia Oceania did Saudi export volumes through 2015’s first three quarters manage to equal 2012’s export volumes. During the same period, Iraq managed to increase its exports to Europe 340,000 barrels per day (data from IEA monthly Oil Market Report).

While they fight for market share in China, the Saudis also have to fight for market share in the established, slow-growing or stagnant IEA-member markets (generally OECD member countries). Saudi exports to these markets declined 310,000 barrels per day between 2012 and 2014, and 490,000 barrels per day between 2012 and 2015’s first three quarters. Only in Asia Oceania did Saudi export volumes through 2015’s first three quarters manage to equal 2012’s export volumes. During the same period, Iraq managed to increase its exports to Europe 340,000 barrels per day (data from IEA monthly Oil Market Report).

It is therefore not surprising that the Saudis moved aggressively in Europe in 4Q 2015—successfully courting traditional Russian customers in Northern Europe and Eastern Europe and drawing complaints from Rosneft.

As with China, the competition will intensify with Iran’s liberation from UN sanctions. For example, Iran has promised to regain its pre-UN sanctions European market share—which implies an increase in exports into the stagnant European market of 970,000 barrels per day (2011’s 1.33 million barrels per day minus 2015’s 360,000 barrels per day).

Might the U.S. be an Ally?

Without unlimited crude export resources, the Saudis have had to choose in which global markets to conduct their market share war, and therefore, implicitly, against which competitors to direct their crude exports.

Why did the Saudis ignore the U.S. market? First, U.S. crude does not represent a threat to the Saudis’ other crude export markets. Until late 2015, when the U.S. Congress passed, and President Obama signed, legislation lifting the prohibition, U.S. producers, with limited exceptions, could not export crude. Even with the prohibition lifted, it is unlikely the U.S. will become a significant competitor, given that the U.S. is a net crude importer. Therefore, directing crude to the U.S. would not improve the Saudi competitive position elsewhere.

Second, the U.S. oil industry is one of the least vulnerable (if not the least vulnerable) to Saudi pressure—and therefore least likely and less quickly to crack. Low production costs are a competitive advantage, but are not the only one and perhaps not the most important one. Financing, technology, equipment, and skilled manpower availability is important, as are political stability, physical security, a robust legal framework for extracting crude, attractive economics, and access and ease of access to markets. The Saudis major export competitors—Russia, Iran, and Iraq—are far weaker than the U.S. on all these areas, as are its minor export competitors, including those within—Nigeria, Libya, Venezuela, and Angola—and outside OPEC—Brazil.

Third, in the U.S. market, the Saudis face tough, well-managed domestic competitors, and a foreign competitor, Canada, that enjoys multiple advantages including proximity, pipeline transport, and trade agreements, the Saudis do not enjoy.

Finally, the Saudis may be focused on gaining a sustainable long term advantage in a different market than the global crude export market—the higher value added and therefore more valuable petroleum product market. Saudi Aramco has set a target to double its global (domestic and international) refining capacity to 10 million barrels per day by 2025. Depressed revenues from crude will squeeze what governments have to spend on their oil industries and, presumably, they will have to prioritize maintaining crude output over investments in refining.

In this Saudi effort, the U.S. could be an ally. The U.S. became a net petroleum product exporter in 2012 (minus numbers in the table below indicate net exports), and net exports grew steadily through 2015. Growth continued in January, with net product exports averaging 1.802 million barrels per day, and, in the week ending February 5, 2.046 million. U.S. exports will lessen the financial attractiveness of investment in domestic refining capacity, both for governments and for foreign investors in their countries’ oil industries (data from EIA).

Saudi Intentions

The view that the Saudi market share strategy is focused on crushing the U.S. shale industry has led market observers obsessively to await the EIA’s weekly Wednesday petroleum status report and Baker-Hugh’s weekly Friday U.S. rig count—and to react with dismay as U.S. rig count has dropped, but production remained resilient.

In fact, they might be better served welcoming resilient U.S. production. It may be that the Saudis will not change course until Russian output declines, Iraq’s stagnates, Iran’s output growth is stunted—and that receding output from weaker countries within and outside OPEC would not be enough. If this is case, the Saudis will see resilient U.S. production as increasing pressure on their competitors and bringing forward the day when they can contemplate moderating their output.

No comments:

Post a Comment